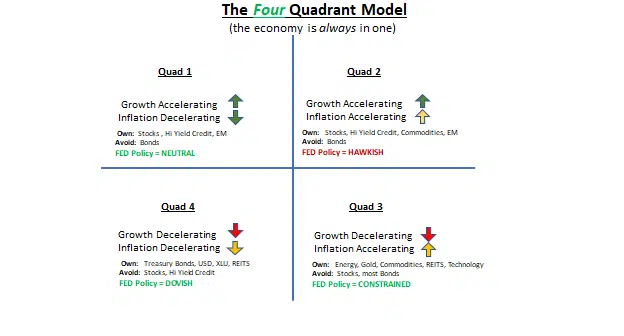

The year 2021 was mostly a Quad 2 year. For those of you unfamiliar with our terminology, that’s when Growth and Inflation are both accelerating. The economy does well under these conditions and stocks love it. So that’s why 2021 was a good year for almost all...

An elderly carpenter was ready to retire. He told his employer contractor of his plans to leave the home building business and live a more leisurely life with his wife and extended family. He would miss his paycheck, but he needed to retire. They could get by. The...

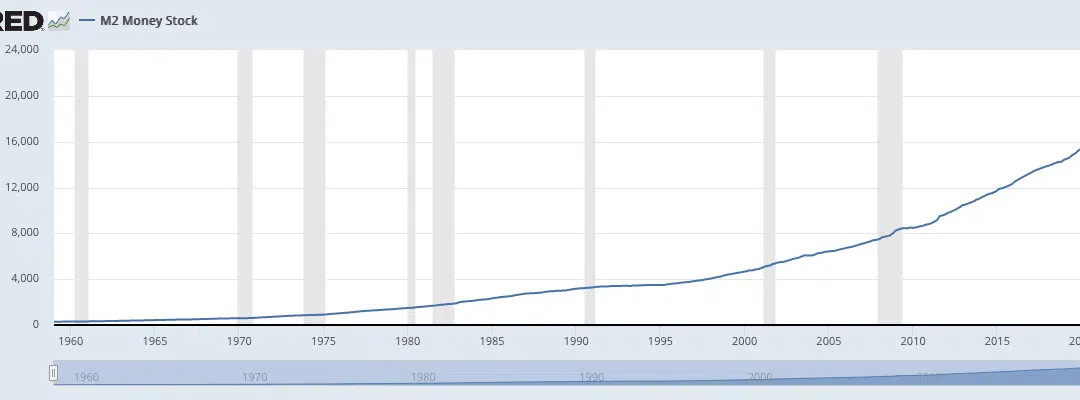

By now, I’m sure you have noticed how the cost of almost everything is rising: housing, food, rent, energy, lumber, gasoline, copper, meat, insurance, corn…even burlap and tallow…almost everything is rising. You may also be wondering how all of this...

It’s the end of the first quarter so I want to provide you with an economic and portfolio update. We have been tracking Quad 2 (see chart above) since the fourth quarter of 2020. Quad 2 is when growth and inflation are accelerating. In this economic regime we want...

If you have retirement savings, then you better have a risk management process for not losing it. Anyone who has a portion of their money invested in an international stock mutual fund with exposure to countries such as China, Germany, South Korea, Italy, Brazil,...